18 months ago, we launched our campaign to engage companies that lack ethnic diversity on their boards. In this blog, we look at the progress achieved to date.

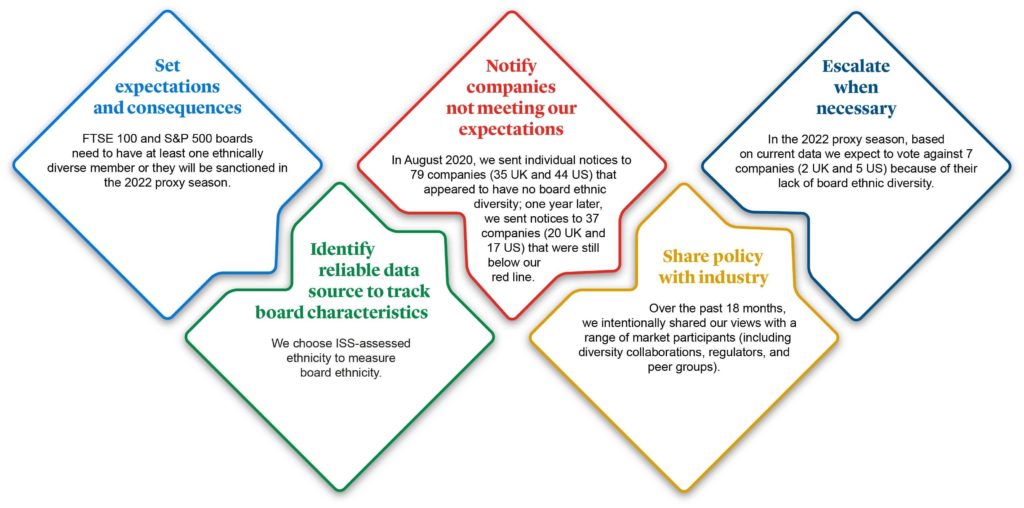

In August 2020, we announced our minimum expectations for ethnic diversity on corporate boards. We did so because we believe more diverse views create better boards, and we began our engagement campaign by focusing on the largest UK- and US-based companies.

We took a straightforward five-step approach:

We name those seven companies below – and will also pre-disclose our voting intentions and rationale a few weeks before their AGM – but before that let’s review the results of our campaign so far.

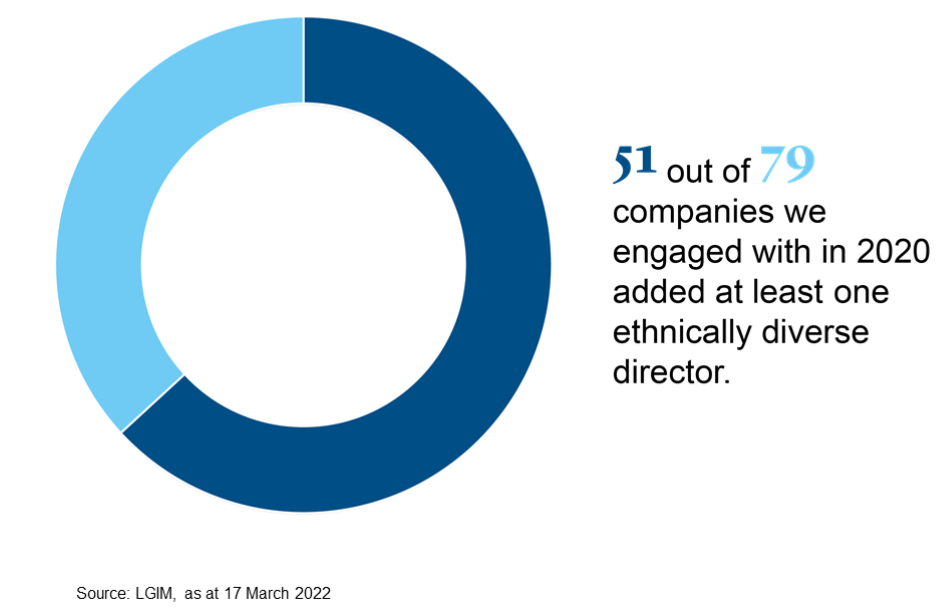

Of the 79 companies we engaged in 2020, 51 have added at least one ethnically diverse director since September 2020 (with a total of 54 individual ethnically diverse directors added).

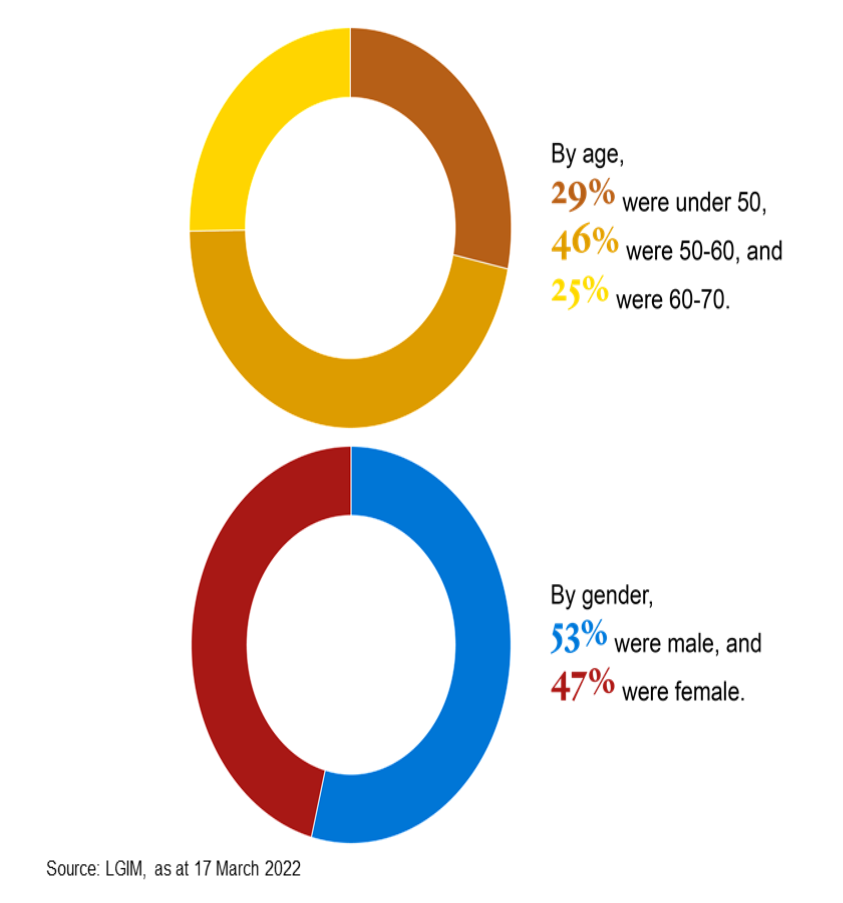

65% of these new directors hold no other public board positions (20% hold one other board seats, and 15% hold two or more), a very encouraging expansion of the universe of board talent.

The campaign also spurred an improvement in the data on this issue. 15 of the 79 companies we engaged were incorrectly listed by third-party providers as lacking ethnic diversity on their boards, and subsequently updated the records.

While there is still evidently much to be done, we are pleased with this progress. As we argued in our original article on this topic, our view is that improving diversity in all its forms is financially material; we believe more diverse organisations make better strategic decisions, show superior growth and innovation, and exhibit lower risk.

The other D&I – data and influence

At the same time, we must also recognise two recurring themes for better stewardship illustrated by this experience: the importance of data and market-wide influence.

Data

Identifying the right data provider is essential. Diversity data are notoriously sensitive, and ethnic diversity data are particularly elusive! We acknowledged from the start that the data were not perfect, but we deemed this too crucial an issue to wait.

That said, despite the misconception that diversity data are highly flawed, we found only a handful of companies had been mislabelled (the aforementioned 15 out of 79). This often had to do with the precise methodology of data collection, and the location and type of company disclosure.

We needed to be willing to understand and explain the minutia of the data methodology, and to be flexible. For example, through the course of the engagement we uncovered outlier examples from which we learned.

A few companies claimed to have ethnic diversity at the aggregate board level, but director-level assessed ethnic diversity data indicated they had none. This made us reflect on the centrality of transparency to stewardship activities.

Ultimately, in these rare but important examples, we accepted the company disclosure but will keep an eye on how the Institutional Shareholder Services (ISS) data evolve.

Influence

Secondly, we saw the value of market influence and collaboration. We would never be so bold as to claim direct and sole credit for driving diversity at the 51 companies that added a director over the past 18 months. Almost all engagement activities are a combination of formal and informal collaboration and influence to drive an outcome.

As soon as we established our policy, we shared it with a broad range of market actors who were working on their own positions. These included diversity coalitions (30% Coalition, 30% Club), regulators, clients, peers and executive-search firms.

There was also a series of highly influential market signals in the first six months that increased the visibility of this issue. In November 2020, for example, ISS updated its benchmark proxy voting and specifically took a position on ethnic board diversity for the first time.

Then, in December 2020, NASDAQ proposed a board diversity rule that included ethnic diversity, which was ultimately approved in August of 2021. We commented on this rule at the time, as did many industry participants. Finally, many of our asset-management peers and clients (the ultimate asset owners) established thoughtful ethnic diversity positions.

All of this has together helped to drive the measurable progress over the past year and a half.

What next?

As noted above, based on current data, in the 2022 proxy season we expect to vote against seven companies (two UK and five US) because of their lack of board ethnic diversity. These companies are:

- DS Smith Plc* (FTSE 100)

- EVRAZ Plc** (FTSE 100)

- IPG Photonics Corporation (S&P 500)

- Mohawk Industries, Inc. (S&P 500)

- People’s United Financial, Inc. (S&P 500)

- Skyworks Solutions, Inc. (S&P 500)

- Universal Health Services, Inc. (S&P 500)

The campaign is far from over, though. We have already informed these companies of our voting intentions, and in the coming months you will see us publicly pre-announce our voting intentions for these companies, amplifying the message across the whole market.

Beyond that, as we have done for gender diversity on boards, we plan to extend our expectations to other regions and to smaller companies. There is much more to be done, and much more to come from us!

*DS Smith – on 9 March 2022, the company announced the appointment of a new director of ethnic minority background, effective 1 June 2022, which is anticipated to meet our expectations.

**EVRAZ Plc – on 11 March 2022, all directors resigned from the board, with the exception of the CEO, with immediate effect. LGIM will monitor the resolutions at the company’s AGM later in the year in order to apply a vote where appropriate.